The Product Lifecycle Management (PLM) market is experiencing notable growth across various sectors such as aerospace and defense, automotive, electronics, and pharmaceuticals. In 2024, over 72% of large manufacturing companies reported the use of PLM software to manage their product data and engineering processes. PLM systems are designed to streamline every phase of a product’s life—from concept to disposal—thereby enhancing efficiency, collaboration, and compliance. More than 45% of companies adopted PLM platforms to improve time-to-market for their products. The automotive and transportation sector represented a major application area, contributing to over 28% of PLM deployments globally. Cloud-based PLM solutions witnessed a 36% rise in adoption in 2023 due to increasing demand for real-time collaboration. The integration of IoT and AI technologies into PLM systems is further driving their adoption, with approximately 41% of new installations incorporating advanced analytics.

Is the Product Lifecycle Management (PLM) Market a Strategic Investment Choice for 2025–2033 ?

Product Lifecycle Management (PLM) Market – Research Report (2025–2033) delivers a comprehensive analysis of the industry’s growth trajectory, with a balanced focus on key components: historical trends (20%), current market dynamics (25%), and essential metrics including production costs (10%), market valuation (15%), and growth rates (10%)—collectively offering a 360-degree view of the market landscape. Innovations in Product Lifecycle Management (PLM) Market Size, Share, Growth, and Industry Analysis, By Type (Cloud-based, On-premises), By Application (Aerospace and Defense, Automotive and Transportation, Medical Devices and Pharmaceutical, Electronics and Semiconductors, Other), Regional Insights and Forecast to 2033 are driving transformative changes, setting new benchmarks, and reshaping customer expectations.

These advancements are projected to fuel substantial market expansion, with the industry expected to grow at a CAGR of 6.8% from 2025 to 2033.

Our in-depth report—spanning over 101 Pages delivers a powerful toolkit of insights: exclusive insights (20%), critical statistics (25%), emerging trends (30%), and a detailed competitive landscape (25%), helping you navigate complexities and seize opportunities in the Services sector.

Global Product Lifecycle Management (PLM) market size is estimated at USD 72863.06 million in 2024 and expected to rise to USD 131946.22 million by 2033, experiencing a CAGR of 6.8%.

The Product Lifecycle Management (PLM) market is projected to experience robust growth from 2025 to 2033, propelled by the strong performance in 2024 and strategic innovations led by key industry players. The leading key players in the Product Lifecycle Management (PLM) market include:

- Autodesk

- Oracle

- Aras

- PTC

- SAP

- Arena PLM

- Hewlett-Packard

- Accenture

- Siemens

- Dassault Systems

- IBM

Request a Sample Copy @ https://www.marketgrowthreports.com/enquiry/request-sample/108941

Emerging Product Lifecycle Management (PLM) market leaders are poised to drive growth across several regions in 2025, with North America (United States, Canada, and Mexico) accounting for approximately 25% of the market share, followed by Europe (Germany, UK, France, Italy, Russia, and Turkey) at around 22%, and Asia-Pacific (China, Japan, Korea, India, Australia, Indonesia, Thailand, Philippines, Malaysia, and Vietnam) leading with nearly 35%. Meanwhile, South America (Brazil, Argentina, and Colombia) contributes about 10%, and the Middle East & Africa (Saudi Arabia, UAE, Egypt, Nigeria, and South Africa) make up the remaining 8%.

The PLM market is evolving rapidly due to the increasing need for digital transformation and operational efficiency. In 2023, over 63% of manufacturing firms prioritized digitalization of their product development processes. Cloud-based solutions are reshaping PLM deployment; adoption of cloud-based PLM platforms increased from 31% in 2022 to 38% in 2024. This transition is fueled by cost efficiency, remote collaboration, and reduced infrastructure overheads.

Another emerging trend is the integration of PLM with enterprise systems such as ERP, MES, and CRM. Around 56% of PLM implementations in 2024 featured integrations with at least one enterprise software. This interoperability allows businesses to establish a seamless data flow across product-related operations. Artificial intelligence and machine learning have also become prominent in enhancing PLM functionalities. As of 2024, over 22% of PLM platforms incorporated predictive analytics and smart automation features. AI-driven PLM systems are aiding in product optimization, defect prediction, and decision-making based on historical design and production data.

The adoption of PLM in the medical devices and pharmaceutical sector surged by 17% between 2022 and 2024. This growth is attributed to stricter regulatory compliance and the need for robust documentation and traceability. Additionally, the electronics and semiconductors segment saw a 14% rise in PLM investments in 2023 due to shrinking product cycles and increasing demand for miniaturization. Sustainability is a growing focus within PLM systems. Around 29% of PLM users integrated lifecycle assessment tools in 2024 to meet environmental regulations and consumer expectations. This trend is especially visible in the European Union, where environmental compliance is strict.

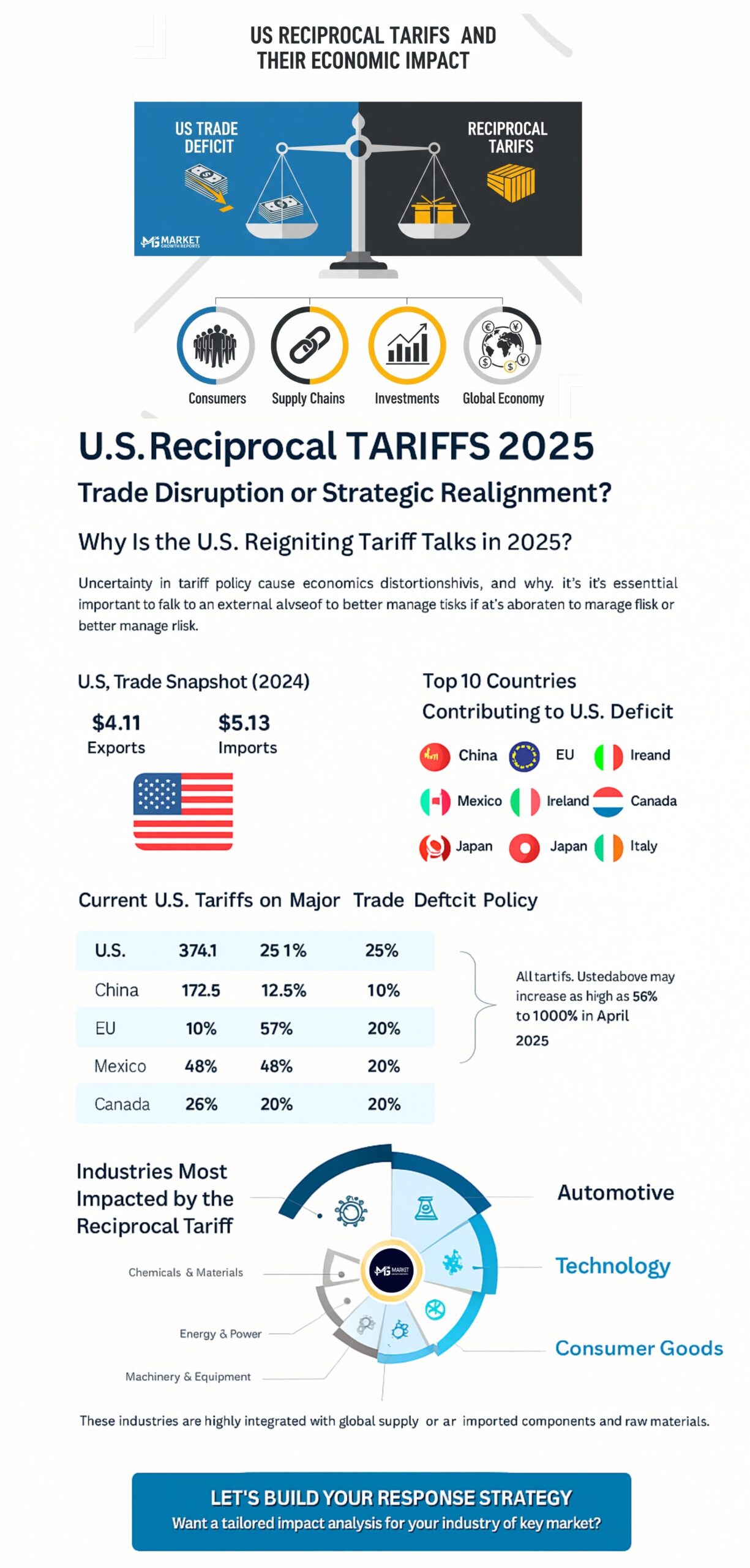

United States Tariffs: A Strategic Shift in Global Trade

In 2025, the U.S. implemented reciprocal tariffs on 70 countries under Executive Order 14257. These tariffs, which range from 10% to 50%, were designed to address trade imbalances and protect domestic industries. For example, tariffs of 35% were applied to Canadian goods, 50% to Brazilian imports, and 25% to key products from India, with other rates on imports from countries like Taiwan and Switzerland.

The immediate economic impact has been significant. The U.S. trade deficit, which was around $900 billion in recent years, is expected to decrease. However, retaliatory tariffs from other countries have led to a nearly 15% decline in U.S. agricultural exports, particularly soybeans, corn, and meat products.

U.S. manufacturing industries have seen input costs increase by up to 12%, and supply chain delays have extended lead times by 20%. The technology sector, which relies heavily on global supply chains, has experienced cost inflation of 8-10%, which has negatively affected production margins.

The combined effect of these tariffs and COVID-19-related disruptions has contributed to an overall slowdown in global GDP growth by approximately 0.5% annually since 2020. Emerging and developing economies are also vulnerable, as new trade barriers restrict their access to key export markets.

While the U.S. aims to reduce its trade deficit, major surplus economies like the EU and China may be pressured to adjust their domestic economic policies. The tariffs have also prompted legal challenges and concerns about their long-term effectiveness. The World Trade Organization (WTO) is facing increasing pressure to address the evolving global trade environment, with some questioning its role and effectiveness.

About Us: Market Growth Reports is a unique organization that offers expert analysis and accurate data-based market intelligence, aiding companies of all shapes and sizes to make well-informed decisions. We tailor inventive solutions for our clients, helping them tackle any challenges that are likely to emerge from time to time and affect their businesses.