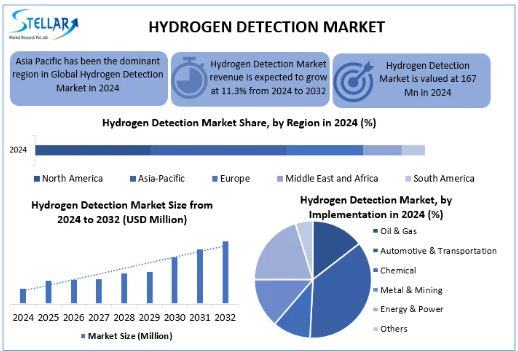

Hydrogen Detection Market was valued at USD 267 million in 2024 and is expected to reach USD 629.16 million by 2032, exhibiting a compound annual growth rate (CAGR) of 11.3% from 2025 to 2032

Market Estimation & Definition

Hydrogen detection systems are technologies used to identify the presence and concentration of hydrogen gas in various environments. These systems are vital in industries like energy, transportation, manufacturing, and chemicals where hydrogen plays a crucial role. The detection systems can be fixed or portable, with a variety of detection technologies ranging from electrochemical to optical.

The Europe Hydrogen Detection Market is currently valued at approximately USD 77.6 million in 2024, and it is projected to grow steadily at a compound annual growth rate (CAGR) of 6.5%, reaching USD 145.8 million by 2034. This robust growth aligns with Europe’s broader efforts to establish itself as a global leader in hydrogen technology, emphasizing safety, efficiency, and innovation.

Market Growth Drivers & Opportunities

Key Drivers

-

Hydrogen Adoption in Industrial & Energy Sectors

The use of hydrogen is rapidly expanding across sectors like steel production, oil refining, chemicals, and energy generation. This increases the risk of gas leaks and necessitates reliable detection systems to maintain safety and compliance. -

Stringent Safety Regulations

European regulatory frameworks are evolving quickly to mandate the use of hydrogen detection systems in new infrastructure, especially in hydrogen fueling stations, electrolysis plants, and distribution hubs. -

Technological Innovations

Advances in sensor design—such as metal-oxide semiconductor (MOS), microelectromechanical systems (MEMS), and optical detection—are improving sensitivity, speed, and durability. These innovations are making hydrogen detection more cost-effective and adaptable to different environments. -

Infrastructure Development

Europe is witnessing rapid development of hydrogen refueling stations and electrolysis facilities, particularly across Germany, France, the Netherlands, and Scandinavia. The growth in infrastructure translates directly into increased demand for hydrogen safety mechanisms.

Key Opportunities

-

Smart Cities and Public Infrastructure

Hydrogen is playing a growing role in public transport and urban heating systems. As these applications grow, so too does the need for comprehensive hydrogen leak detection and monitoring systems. -

Hydrogen-Powered Vehicles

As Europe pushes toward zero-emission transportation, the proliferation of hydrogen-powered vehicles will boost demand for detection systems in vehicles, maintenance stations, and refueling points. -

Green Hydrogen Projects

Europe’s leadership in renewable hydrogen production creates unique opportunities for sensor and detection system suppliers to collaborate with project developers, ensuring that safety is built into the earliest stages of deployment.

Segmentation Analysis

The Europe Hydrogen Detection Market is segmented based on the following:

By Technology

-

Electrochemical Sensors

-

Catalytic Sensors

-

Metal-Oxide Semiconductor (MOS)

-

Thermal Conductivity Sensors

-

MEMS-based Sensors

-

Optical Sensors and Others

Electrochemical and MOS sensors are leading the market due to their cost-efficiency and quick response times.

By Implementation Type

-

Fixed Detection Systems

Installed permanently in industrial plants, storage facilities, and refueling stations. -

Portable Detection Systems

Used for on-site inspections, mobile applications, and personal safety gear. Portable systems currently dominate with a market share of over 69%.

By Application

-

Industrial Processing Units

-

Energy Generation Facilities

-

Transportation Infrastructure

-

Residential and Commercial Buildings

Industrial and energy segments hold the majority share, driven by stringent safety requirements.

By Detection Range

-

0–1,000 ppm

-

0–5,000 ppm

-

0–20,000 ppm

-

Above 20,000 ppm

Systems with detection capabilities in the 0–5,000 ppm range are the most widely used, offering a balance of sensitivity and cost.

Country-Level Analysis

Germany

Germany is the largest market in Europe for hydrogen detection systems, expected to grow at a CAGR of 7.5% through 2034. The country’s ambitious hydrogen roadmap includes investments in green hydrogen production, heavy industry decarbonization, and a vast network of hydrogen refueling stations. These developments are creating a surge in demand for both fixed and portable hydrogen sensors, especially in industrial clusters and logistics corridors.

France

France is experiencing a significant uptick in hydrogen infrastructure projects. Hydrogen-powered public transport, energy storage initiatives, and industrial pilot programs are driving sensor demand. Regulatory incentives and government funding further support safety innovations, contributing to market expansion.

Other European Countries

Countries such as the Netherlands, Sweden, and Spain are emerging as secondary growth hubs. These regions are focused on developing hydrogen valleys—integrated ecosystems of production, storage, and usage—where detection systems will be crucial.

Stakeholder (Commutator) Analysis

End-Users

-

Industrial Facilities:

Refineries, chemical plants, steel manufacturing units require embedded hydrogen detection systems for safety. -

Transportation Networks:

Hydrogen-powered buses, trains, and cargo fleets depend on portable and in-vehicle detection devices.

Manufacturers

-

Sensor Developers:

These include companies producing MEMS, electrochemical, and optical detection technologies. -

OEMs and Assemblers:

Integration of detection modules into control systems, industrial automation platforms, and safety cabinets.

System Integrators

Firms that install and configure safety and monitoring systems across hydrogen infrastructure, often bundling detection with IoT-enabled dashboards or control rooms.

Governments & Regulatory Bodies

Entities shaping safety policies, compliance frameworks, and subsidy schemes. European agencies are leading initiatives on hydrogen readiness and safety mandates.

R&D and Academic Institutions

Institutions across Europe are researching next-gen detection materials like palladium-based alloys, nanostructured semiconductors, and wireless sensing networks for smart manufacturing environments.

Investors & Project Developers

Private equity firms, venture capitalists, and corporate developers of hydrogen facilities are increasingly including safety technology in their capital allocation frameworks.

Conclusion

The Europe Hydrogen Detection Market stands at a critical inflection point. Valued at USD 77.6 million in 2024 and set to nearly double to USD 145.8 million by 2034, the market reflects the continent’s strategic shift toward a hydrogen-based, low-emission economy.

Hydrogen safety is not a peripheral concern—it is foundational. As infrastructure scales, the reliability and responsiveness of detection systems will determine the pace and public acceptance of hydrogen technologies. Leading countries like Germany and France are setting benchmarks in detection adoption, but other nations are quickly following suit.

About Stellar Market Research:

Stellar Market Research is a multifaceted market research and consulting company with professionals from several industries. Some of the industries we cover include science and engineering, electronic components, industrial equipment, technology, and communication, cars, and automobiles, chemical products and substances, general merchandise, beverages, personal care, and automated systems. To mention a few, we provide market-verified industry estimations, technical trend analysis, crucial market research, strategic advice, competition analysis, production and demand analysis, and client impact studies.

Contact Stellar Market Research:

S.no.8, h.no. 4-8 Pl.7/4, Kothrud,

Pinnac Memories Fl. No. 3, Kothrud, Pune,

Pune, Maharashtra, 411029

+91 20 6630 3320, +91 9607365656